Interaction Design

Choosing the right AI interaction model

Financial decisions require both speed and trust. Three models were evaluated before selecting the approach that best balanced those needs.

Interface Agent

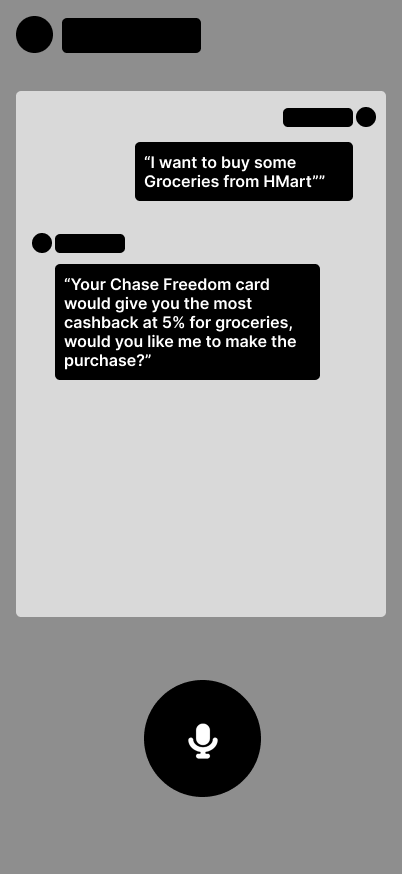

User speaks in natural language; AI interprets and acts. Fast and accessible, but opaque — users who want to compare alternatives have no visibility into the reasoning.

Direct Manipulation

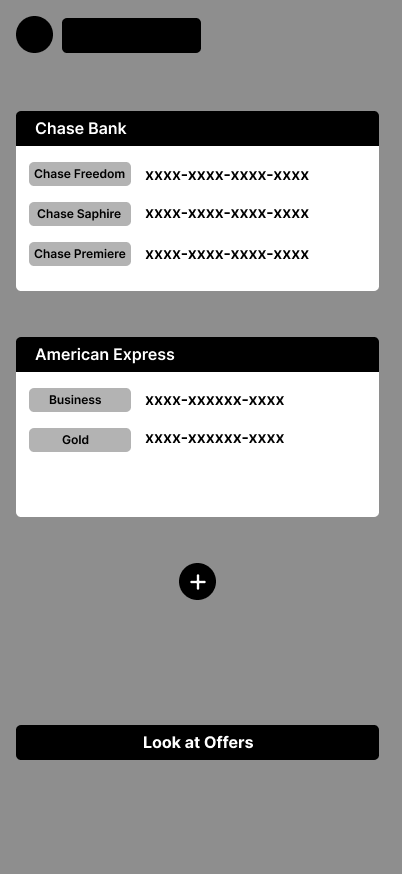

Users control filters, rankings, and card views directly. Maximum transparency, but high cognitive load — less financially savvy users found this overwhelming.

Selected

Mixed Initiative

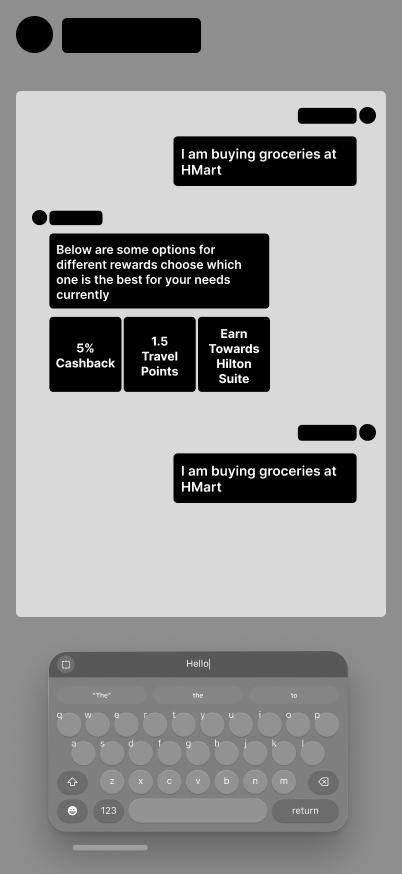

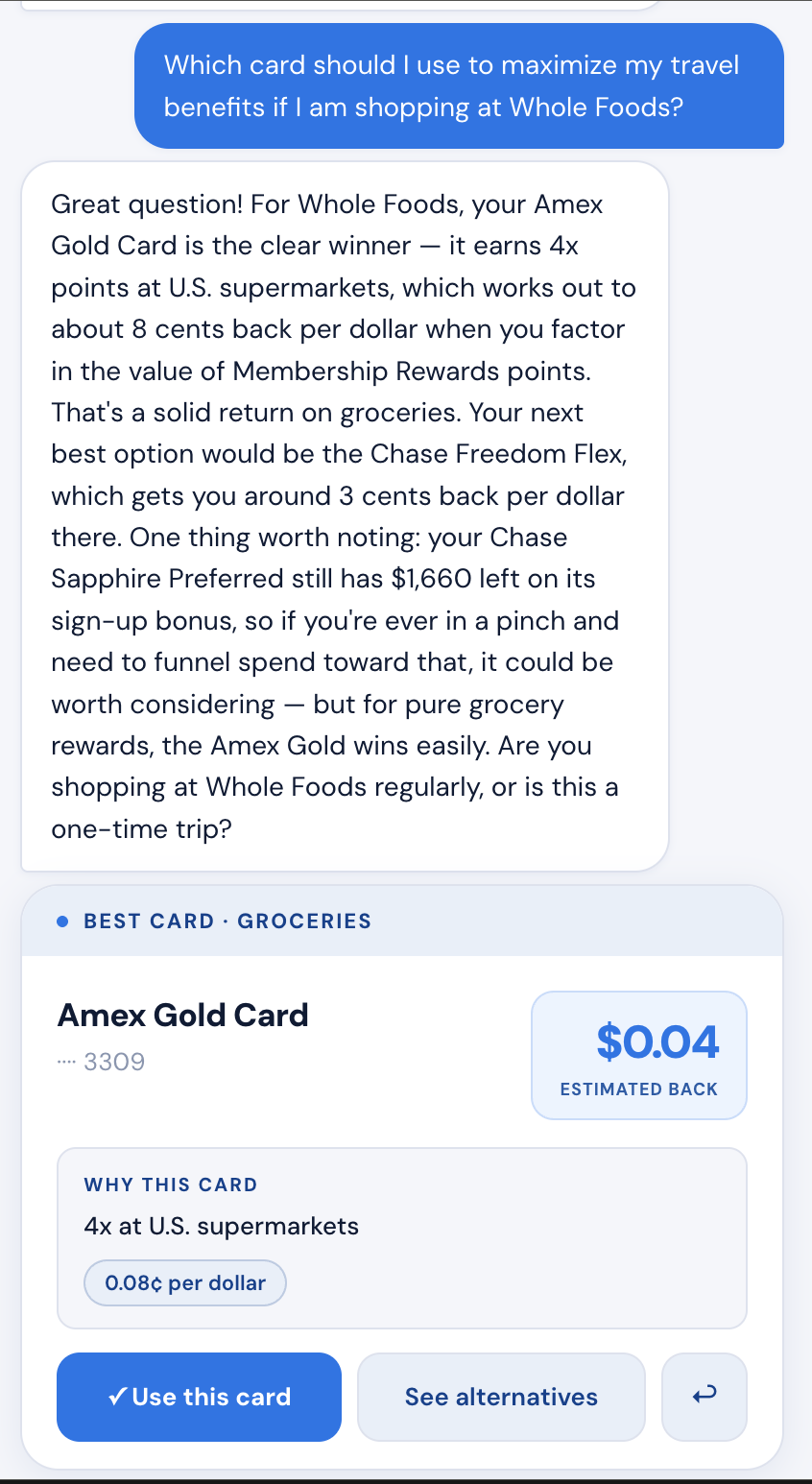

AI proactively surfaces recommendations; users retain final say and can adjust preferences at any point. Balances efficiency with trust — critical in financial contexts.

The final design also pulls from Direct Manipulation — a card gallery view lets users scan all options at a glance without needing to converse with the AI when they just want the data fast.

Lo-fi Wireframes

Voice Interface Agent

Mixed Initiative Interaction

Direct Manipulation Agent